Decoding The Ohio Division Of Agriculture’s Chart Of Accounts: A Deep Dive Into Monetary Transparency

Decoding the Ohio Division of Agriculture’s Chart of Accounts: A Deep Dive into Monetary Transparency

Associated Articles: Decoding the Ohio Division of Agriculture’s Chart of Accounts: A Deep Dive into Monetary Transparency

Introduction

On this auspicious event, we’re delighted to delve into the intriguing matter associated to Decoding the Ohio Division of Agriculture’s Chart of Accounts: A Deep Dive into Monetary Transparency. Let’s weave fascinating data and provide recent views to the readers.

Desk of Content material

Decoding the Ohio Division of Agriculture’s Chart of Accounts: A Deep Dive into Monetary Transparency

The Ohio Division of Agriculture (ODA), chargeable for safeguarding the state’s agricultural business and making certain the security of its meals provide, operates below a fancy monetary construction. Understanding this construction requires familiarity with its Chart of Accounts (COA), an in depth itemizing of all of the accounts used to document monetary transactions. Whereas the ODA’s particular COA is not publicly accessible in a readily digestible format like a downloadable spreadsheet, analyzing publicly accessible monetary experiences and finances paperwork permits us to glean worthwhile insights into its organizational construction and spending priorities. This text goals to offer a conceptual understanding of the doubtless elements and construction of the ODA’s COA, drawing parallels with frequent governmental accounting practices.

Understanding Governmental Chart of Accounts:

Earlier than delving into the specifics of the ODA, it is essential to know the overall ideas governing governmental COAs. These charts usually comply with a standardized construction, typically based mostly on Typically Accepted Accounting Rules (GAAP) for presidency entities, or modifications thereof. Key traits embrace:

-

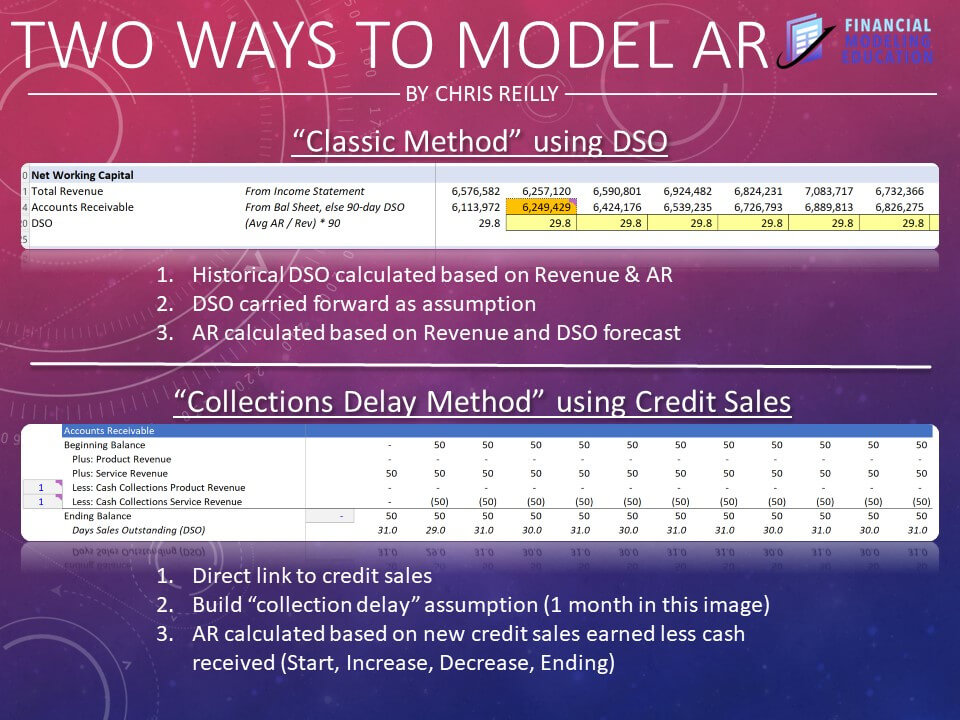

Fund Accounting: Governmental entities typically use fund accounting, separating monetary assets into distinct funds based mostly on their objective (e.g., common fund, particular income funds, capital tasks funds, debt service funds, enterprise funds). This segregation ensures accountability and transparency for particular tasks and actions. The ODA doubtless employs this method, with funds devoted to numerous applications like meals security inspections, agricultural analysis, and regulatory enforcement.

-

Object Codes: Every fund is additional damaged down utilizing object codes, which categorize expenditures by kind (e.g., personnel companies, provides, gear, journey, contracts). This degree of element permits for granular evaluation of spending patterns inside every fund.

-

Program Codes: Many governmental COAs incorporate program codes to hyperlink expenditures to particular applications or initiatives. For the ODA, this would possibly embrace applications associated to pesticide regulation, livestock well being, agricultural advertising and marketing, or soil and water conservation.

-

Exercise Codes: An extra layer of element would possibly contain exercise codes, distinguishing between varied actions inside a program. For instance, a pesticide regulation program might need actions like inspections, licensing, and enforcement.

-

Useful Codes: This degree categorizes expenditures based mostly on the operate they serve inside the company’s total mission. Examples for the ODA may embrace regulatory companies, analysis and growth, schooling and outreach, and administrative assist.

Probably Elements of the ODA’s Chart of Accounts:

Primarily based on the ODA’s publicly accessible data and customary governmental accounting practices, we will infer the doubtless elements of its COA:

-

Common Fund: This fund would doubtless cowl the ODA’s day-to-day working bills, together with salaries, administrative prices, and common program assist.

-

Particular Income Funds: These funds would account for particular income sources devoted to specific applications. Examples may embrace funds acquired from pesticide registration charges, grants for agricultural analysis, or charges collected for livestock inspections. Every particular income fund would have its personal set of object, program, and exercise codes reflecting the particular objective of the funding.

-

Capital Tasks Funds: These funds would monitor expenditures associated to the acquisition or development of capital belongings, resembling new laboratory gear, workplace buildings, or agricultural analysis services.

-

Enterprise Funds: Whereas much less more likely to be distinguished, enterprise funds would possibly exist if the ODA operates any self-supporting actions, resembling a state-run agricultural testing laboratory producing income by means of its companies.

Analyzing ODA Monetary Stories:

Whereas the detailed COA is not publicly accessible, analyzing the ODA’s annual finances and monetary experiences offers insights into its spending patterns. These experiences usually summarize expenditures by fund, program, or object classes, providing a high-level view of the monetary exercise mirrored within the underlying COA. By inspecting these experiences, we will establish key spending areas and monitor adjustments over time. As an example, we will observe traits in spending on personnel, gear, regulatory actions, or analysis initiatives.

Challenges and Alternatives:

Accessing and understanding the complete element of the ODA’s COA presents challenges. The shortage of a publicly accessible, detailed COA limits the power for impartial evaluation and oversight. Nonetheless, the ODA’s dedication to transparency, as demonstrated by means of its publicly accessible monetary experiences, is a constructive step. Enhancing accessibility to the COA, doubtlessly by means of a simplified on-line portal or a extra detailed rationalization of the coding system utilized in its monetary experiences, would tremendously improve public understanding and accountability.

Conclusion:

The Ohio Division of Agriculture’s Chart of Accounts is a fancy however important software for managing and monitoring its monetary assets. Whereas the complete COA is not publicly accessible, understanding the ideas of governmental accounting and analyzing publicly accessible monetary experiences permits for an affordable interpretation of the ODA’s spending priorities and monetary construction. Elevated transparency, notably by means of enhanced entry to the COA particulars, would foster better public belief and accountability within the administration of public funds devoted to Ohio’s important agricultural sector. Future efforts to enhance accessibility and supply clearer explanations of the coding construction utilized in ODA monetary experiences would considerably profit researchers, stakeholders, and the general public alike. This might facilitate a extra complete understanding of the ODA’s monetary operations and its impression on the state’s agricultural panorama.

:max_bytes(150000):strip_icc()/chart-accounts-4117638b1b6246d7847ca4f2030d4ee8.jpg)

Closure

Thus, we hope this text has supplied worthwhile insights into Decoding the Ohio Division of Agriculture’s Chart of Accounts: A Deep Dive into Monetary Transparency. We admire your consideration to our article. See you in our subsequent article!